Why building more homes won’t solve the affordable housing problem

The problem isn't the supply of housing; it's that millions of people lack the income to afford what’s on the market.

Even before 2020, the United States faced an acute housing affordability crisis. The COVID-19 pandemic made it a whole lot worse after millions of people who lost their jobs fell behind on rent. While eviction bans forestalled mass homelessness — and emergency rental assistance has helped some — most moratoriums have now been lifted, putting a lot of people at risk of losing their homes.

One solution pushed by the White House, state and local lawmakers, and many others is to increase the supply of affordable housing, such as by reforming zoning and other land-use regulations.

As experts on housing policy, we agree that increasing the supply of homes is necessary in areas with rapidly rising housing costs. But this won’t, by itself, make a significant dent in the country’s affordability problems — especially for those with the most severe needs.

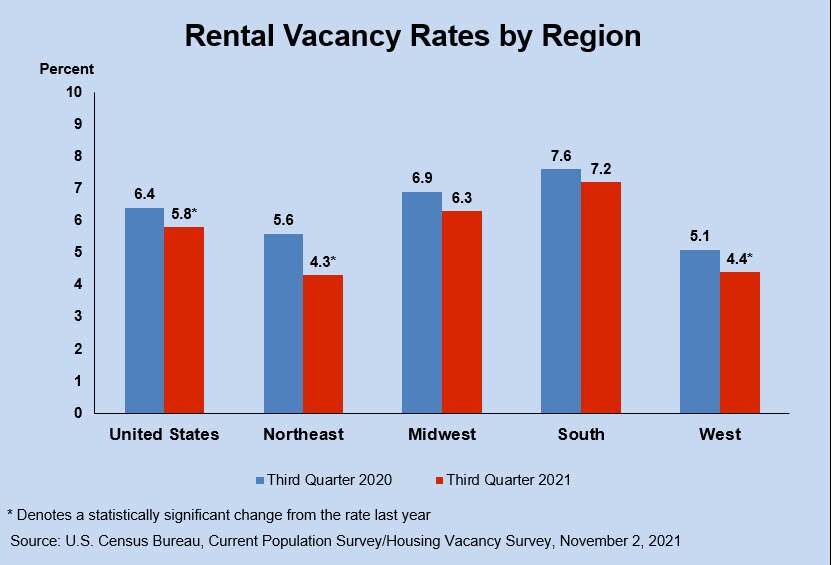

In part that’s because in much of the country, there is actually no shortage of rental housing. The problem is that millions of people lack the income to afford what’s on the market.

{kind=link}

Where the crisis hits hardest

Renters with the most severe affordability problems have extremely low incomes.

Nationally, about 45% of all renter households spend more than 30% of their pretax income on rent — the widely recognized threshold of affordability. About half of these renters, 9.7 million in total, spend more than 50% of their income on housing, greatly impairing their ability to meet other basic needs and putting them at risk of becoming homeless.

Nearly two-thirds of renters paying at least half of their income on housing earn less than $20,000, which is below the poverty line for a family of three. Renters with somewhat higher incomes also struggle with housing affordability, but the problem is most pervasive and most severe among very-low income households.

For a household earning $20,000, $500 per month is the highest affordable rent, assuming the affordability standard of spending no more than 30% of income on housing. In contrast, the median rent in the U.S. in 2019 was $1,097, a level that’s affordable to households earning no less than $43,880.

And homes that rent for $500 or less are exceedingly scarce. Fewer than 10% of all occupied and vacant housing units rent for that price, and 31% are occupied by households earning more than $20,000, pushing low-income renters into housing they cannot afford.

A pervasive problem

The problem of housing affordability doesn’t affect only a few high-cost cities. It’s pervasive throughout the nation, in the priciest housing markets with the lowest vacancy rates like New York and San Francisco, and the least expensive markets with high vacancy rates, such as Cleveland and Memphis.

For example, in Cleveland, with a median rent of $725, 27% of all renters spend more than half of their income on rent. In San Francisco, with a median rent of $1,959, 18% of renters spend at least half their income on rent. And it’s even worse for the poorest residents. In both cities, more than half of all extremely low-income renters spend at least 50% of their income on rent.

In fact, there is not a single state, metropolitan area, or county in which a full-time minimum-wage worker can afford the “fair market rent” for a two-bedroom home, as designated by the U.S. Department of Housing and Urban Development.

Even the smallest, most basic housing units are often unaffordable to people with very low incomes. For example, the minimum rent necessary to sustain a new a 225-square-foot efficiency apartment with a shared bathroom in New York City built on donated land is $1,170, affordable to households earning a minimum of $46,800. That’s way out of reach for low-income households.

At the heart of the nation’s affordability crisis is the fact that the cost to build and operate housing simply exceeds what low-income renters can afford. Nationally, the average monthly operating cost for a rental unit in 2018 was $439, excluding mortgage and other debt-related expenses.

In other words, even if landlords set rents at the bare minimum needed to cover costs — with no profit — housing would remain unaffordable to most very-low-income households — unless they also receive rental subsidies.

The subsidy solution

Covering the difference between what these renters can afford and the actual cost of the housing, then, is the only solution for the nearly 9 million low-income households that spend at least half their income on rent.

The U.S. already has a program designed to help these people afford homes. With Housing Choice Vouchers, also known as Section 8, recipients pay 30% of their income on rent, and the program covers the balance. While some landlords have refused to accept tenants using vouchers, overall the program has made a meaningful difference in the lives of those receiving them.

The $26 billion program currently serves about 2.5 million households, or only 1 in 4 of all eligible households. The version of the Democrats’ social spending bill passed by the House of Representatives included about $25 billion to expand the program.

While this would be the single largest increase in the program’s nearly 50-year history, it would still leave millions of low-income renters unable to afford a home. And that’s not a problem more supply can solve.

Alex Schwartz, a professor of urban policy at The New School, is the author of “Housing Policy in the United States” (Routledge, 2021). He is a public member of the New York City Rent Guidelines Board. Kirk McClure, a professor of urban planning at the University of Kansas, receives funding and a data license from the U.S. Department of Housing and Urban Development. This article is republished from The Conversation under a Creative Commons license.